How the Strait of Hormuz Blockade is Transforming Credit Access in 2026

The blockade of the Strait of Hormuz has profoundly disrupted global supply chains,causing sharp price increases for vital goods such as gasoline and medical equipment. This interruption has led to shortages in essential materials like jet fuel and helium, impacting industries from aviation to energy.Beyond these visible effects, the crisis is subtly reshaping consumer credit availability worldwide.

Geopolitical Strife’s subtle Influence on Lending Practices

the standoff between Iran and the U.S. over this critical maritime passageway is expected to persist intermittently throughout much of 2026. While individual credit scores remain largely unaffected directly by this conflict, financial institutions have quietly tightened their lending standards. Banks are now conducting more thorough evaluations of borrower profiles, making loan approvals more challenging even when applicants’ credit ratings stay consistent.

As an exmaple, a recent analysis from an AI-powered credit platform reveals that obtaining a mortgage with a 670 FICO score today demands far stricter scrutiny than it did just months ago. Many consumers who previously qualified without issue now encounter delays or denials without transparent explanations.

Illustrative Cases Highlight Lending Shifts

A notable example involves an applicant with a solid 690 FICO score and stable employment who was refused an auto loan despite holding $8,000 in savings-a scenario that would have been approved easily last year. Mortgage brokers across various states report similar trends: during periods marked by geopolitical uncertainty,lenders either uphold stringent criteria or increase caution by raising capital reserves and reassessing borrowers once deemed low risk.

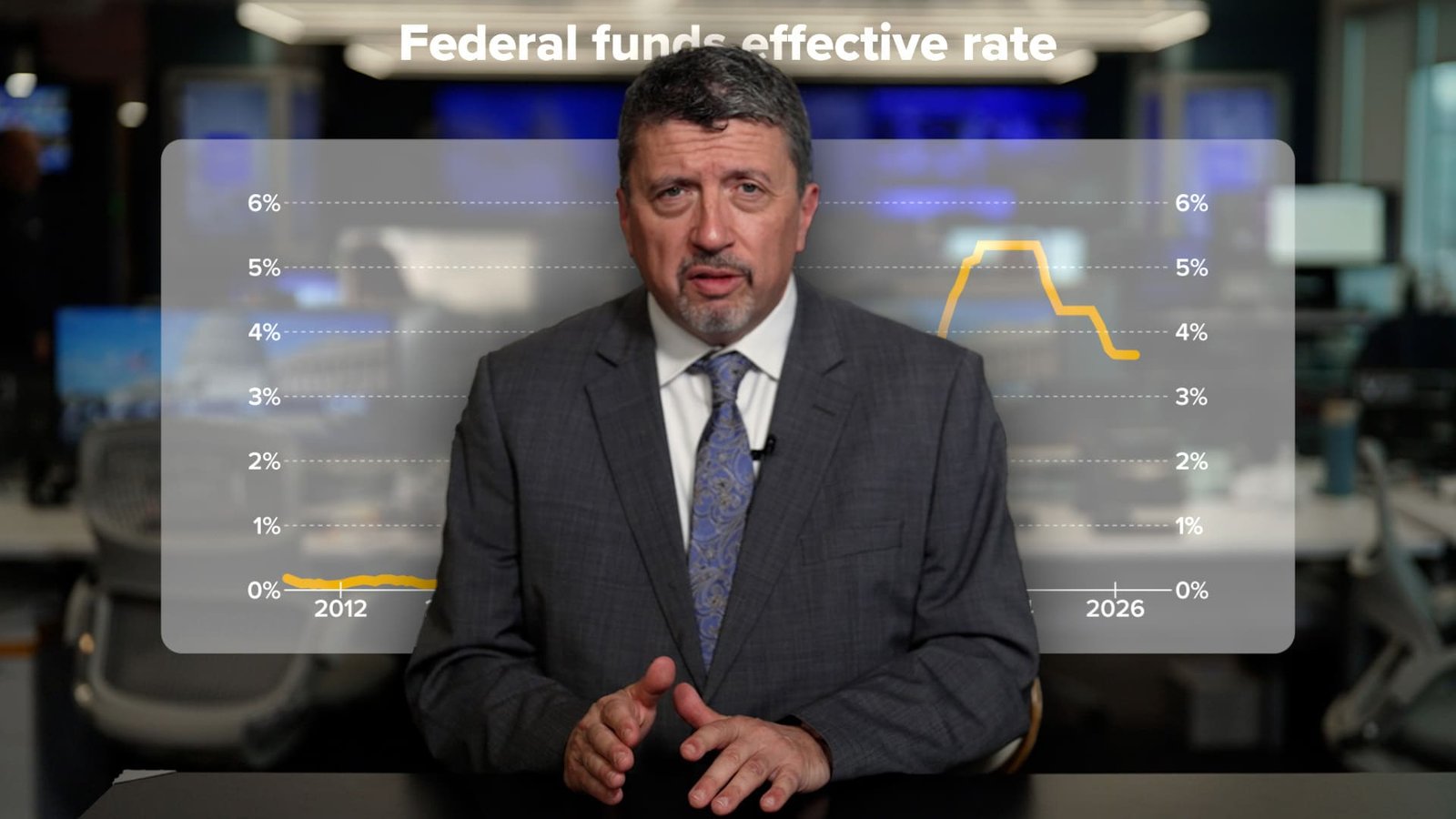

Why Interest Rates Don’t Tell the whole Story

Many consumers anticipated easier borrowing conditions as inflation showed signs of easing early in 2026; however, ongoing geopolitical tensions combined with surging oil prices have complex central bank policies globally. Despite speculation about potential Federal Reserve rate cuts under new leadership later this year, recent meetings maintained steady rates with market forecasts leaning toward stability or slight increases through 2026.

This environment means that even if nominal interest rates fall eventually, access to loans may not improve proportionally as lenders prioritize mitigating risk over lowering rates alone. Borrowers within mid-tier credit brackets (640-700) frequently face additional documentation requests-often serving as indirect rejections rather than outright declines.

The Role Inflation Plays in Heightened Caution

Inflation climbed back up to approximately 3.5% in May-well above target levels-largely fueled by volatile energy costs linked to Middle Eastern instability. Financial experts note that such macroeconomic unpredictability prompts lenders to adopt more conservative approaches when extending credit lines: higher inflation equates to increased perceived risk for banks evaluating loan applications.

“The real cost of borrowing rises when fewer applicants meet elevated qualification standards,” explains an economics professor specializing in financial markets-a phenomenon known as the ‘risk channel,’ where tighter access occurs independently from interest rate movements.”

This dynamic leads many prospective borrowers to abandon applications after encountering extensive paperwork demands rather than facing outright refusals-a trend contributing significantly to reduced loan originations across sectors like automotive financing and home mortgages alike.

Diverse Lender Strategies Amid Market Uncertainty

- Heightened caution: Some mortgage providers have reinstated rigorous guidelines reminiscent of those during extended crises such as COVID-19-requiring higher minimum scores and comprehensive income verification especially for jumbo loans.

- Consistent underwriting: Other institutions maintain steady lending practices based on real-time portfolio data instead of reacting solely on geopolitical developments; they argue capital remains sufficient where core business fundamentals hold firm.

- cautious pullbacks: A smaller segment temporarily reduces lending activity due to perceived risks but risks losing market share as competitors continue operations under disciplined frameworks.

Tactical Guidance for Borrowers Navigating Today’s Credit Environment

- Avoid surprises at request time by thoroughly reviewing detailed credit reports well before applying;

- Eagerly prepare supplementary documents early since lenders increasingly request extensive proof;

- If denied unexpectedly despite strong credentials, seek advice from specialists familiar with evolving underwriting criteria;

- Acknowledge external factors beyond personal control are influencing approval odds more heavily today;

- pursue multiple lender options since policies vary widely amid current uncertainties;

- Mental preparedness helps manage frustration caused by slower processing times or ambiguous responses from banks;

.

The Wider Economic Consequences Looming Ahead

Tighter consumer credit conditions threaten long-term spending patterns since fewer approved mortgages and auto loans translate into diminished household consumption-the engine driving economic growth across nations including the United States.

Industry analysts warn prolonged instability could trigger contractions comparable though not identical in timing or scale compared with pandemic-era disruptions.

“Extended unresolved tensions force global lenders into reassessing their appetite for risk,” one expert notes.

Ultimately while headline interest rate figures dominate news cycles daily-the underlying shifts determining who qualifies for loans reflect deeper economic realities intertwined closely with ongoing geopolitical challenges.

Understanding these complex forces empowers consumers navigating uncertain times marked by fluctuating oil prices alongside persistent international conflicts shaping everyday financial decisions worldwide.

{kind=link}